Manufacturing

The State of Manufacturing in December

Along with the holidays and celebrations, December is a time to reflect and gear up for the new year. As we plan and budget, it’s not only important to look at where we are today, but where we want to be, so we know how to get there. This can be challenging, especially with an economy in flux and at an increased risk of a recession, additional inflationary waves, geopolitical conflict, and slower economic growth. With an eye on the coming year, let’s take a look at the State of Manufacturing and the U.S. Economy.

According to the ISM Manufacturing Purchasing Managers’ Index, the activity for manufacturing contracted for the first time since May 2020 with the index falling to 49.0 in November. Anything below the 50 threshold reflects a shrinking economy, which translates to contracting new orders, falling exports, and declining employment and slowing production. The one silver lining is improvement in supply chain disruptions and challenges.

While consumer prices did rise, the consumer price index fell to 7.1% in November, the lowest level since the end of last year, according to the U.S. Bureau of Labor Statistics. This is compared to 7.7% in October and a high of 9.1% in June. Given this slowing of inflation, Wall Street correctly anticipated the Federal Reserve slowing the pace of increasing interest rates to rein in inflation and prices with a rise in the benchmark rate by half a percentage point (50 basis points), increasing the rate to 4.50%. It is further expected that the Federal Open Market Committee (FOMC) will continue to hike interest rates to between 5 and 5.25% by the end of next year, and not begin reducing interest rates until 2024. In the meantime, it is important to keep in mind that inflation still remains near 40-year record highs and “the areas that saw the largest 12-month increases, according to the U.S. Chamber of Commerce, included food up 10.6%, energy up 13.1%, and housing up 7%.”

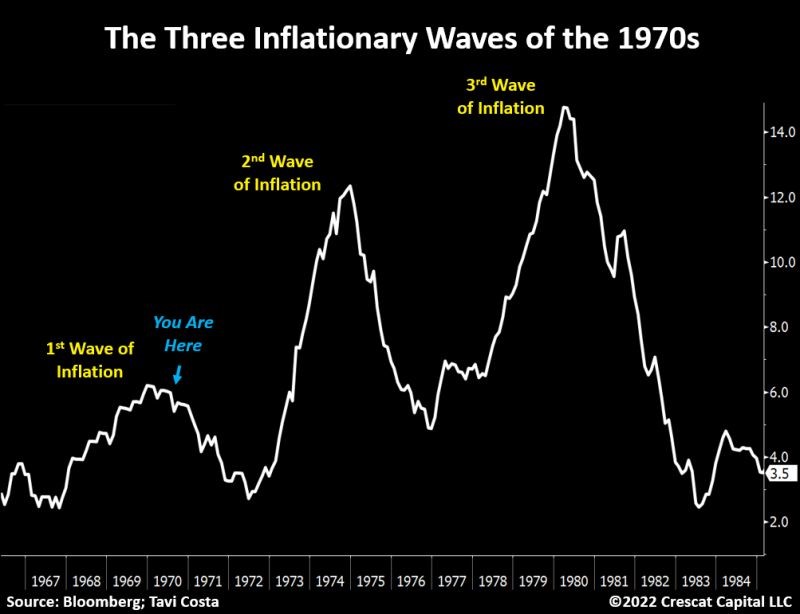

While this slowing trend is moving in the right direction, more work and time is needed to curb high inflation and work out the excess stimulus and liquidity in the system, which, along with surging demand and supply chain and workforce shortages contributed to inflation. It is also worth noting the U.S. experienced waves of inflation in the 1970s and this current moderation or slowing of inflation might be setting the stage for additional inflationary waves. Otavio Costa, Partner and Portfolio Manager at Crescat Capital, views inflation “as a structural problem caused by secular forces, including wage growth, commodity shortages, aggressive fiscal spending, and deglobalization, and that inflation develops through waves, and we have seen the first wave.”

While this time might be different, it may not be and understanding past historical, inflationary trends provides a future potential scenario when planning and when there’s uncertainty.

Tapping Québec for FDIs in Partnership with GlobalFoundries

GlobalFoundries offers both space and an array of amenities for Québec manufacturing companies seeking a U.S. footprint. To capitalize on this market opportunity, the Vermont Chamber, the Vermont Agency of Commerce, GBIC, and CIDEP (Vermont’s foreign trade representative firm in Montréal) are partnering with GlobalFoundries on tenant recruitment efforts to grow Vermont’s $3 billion dollar manufacturing industry. This work supports of the Governor’s economic development priorities to strengthen our ties with Québec and transform Vermont into a Supply Chain Hub. Recruitment of Québec companies in the aerospace and defense sectors also strengthens cross-border commerce and the Vermont Chamber’s work to build the Vermont – Québec Aerospace Trade Corridor.

Vermont Delegation Attends Aerospace Components Manufacturing Tradeshow

In partnership with the Vermont Agency of Commerce, the Vermont Chamber led a delegation of Vermont manufacturers at the recent Aerospace Components Manufacturers (ACM) event in Hartford, CT. This participation was in support of the expansion of the Vermont – Québec Aerospace Trade Corridor into Connecticut. The corridor connects Vermont’s combined $2 billion aerospace and aviation industry with an $18 billion Québec aerospace cluster.

Vermont’s delegates included Concepts NREC, Manufacturing Solutions Inc., and Stephens Precision, who met with Connecticut aerospace and defense suppliers to discuss workforce and new business development opportunities. The delegates also met with many of the 1,200 students who were engaged with the Job Fair component of the event.

As a Trade Corridor partner, ACM suppliers were able to participate in the recent virtual 2022 Manufacturing Summit, where they secured NDAs and approved supplier status with OEMs and primes, including Bell Flight, Lockheed Martin, and SAFRAN.

Vermont Chamber Hosts 9th Annual Manufacturing Summit

Since 2013, the Vermont Chamber of Commerce has convened manufacturing industry leaders at the annual Manufacturing Supply Chain Summit. In recent years, the pandemic prompted the event to go virtual, increasing accessibility for global buyers, suppliers, and partners to engage with Vermont and New England manufacturers and leaders. Due to the success of the virtual model, the event was once again held virtually this year, bringing together representatives from throughout the United States, Canada, and Europe. The 2022 event was themed “Rebuilding Supply Chains and Workforce through Content, Collaboration, and Contacts.”

85 suppliers and 25 OEMs, Primes, and Government Agencies held 300 meetings between buyers, suppliers, and partners, representing hundreds of new connections between participants. Many of the attendees were leaders in the aerospace, aviation, defense, and naval/marine industries.

The event also offered a rich two-day agenda of seminars and roundtable discussions focused on new and emerging trends in advanced manufacturing for the aerospace, aviation, defense, space, industrial, and naval/marine industries. Sessions were moderated by Vermont Chamber Vice President of Business Development, Christopher Carrigan.

“The Vermont Chamber is proud to continue our legacy of championing manufacturing by hosting an event that is a catalyst for collaboration and innovation. A testament to this is the 26 Canadian, 8 Connecticut, and 8 Ontario suppliers in attendance supporting the Vermont Chamber’s work to build the Vermont – Québec Aerospace Trade Corridor that now extends from Connecticut to Ontario,” stated Carrigan. “We’re already looking forward to celebrating a decade of Manufacturing Summits at next year’s event.“

Senator Patrick Leahy and Governor Phil Scott both delivered virtual remarks at the event, celebrating Vermont’s leadership in the manufacturing and aerospace industries, and addressing some of the top challenges facing businesses.

The 2022 Manufacturing Summit was made possible by our sponsors:

To join us as a sponsor for the 2023 Manufacturing Summit, please contact Chris Carrigan: (802) 223-0904, ccarrigan@vtchamber.com.

Vermont Delegation Champions International Collaboration, Manufacturing, at Aerospace Innovation Forum

In partnership with the Vermont Agency of Commerce and U.S. Commercial Service, the Vermont Chamber hosted a delegation of Vermont aerospace companies at Aéro Montréal’s 2022 Aerospace Innovation Forum. This work was in support of the Vermont Chamber’s ongoing commitment to building the Vermont – Québec’s Aerospace Trade Corridor to connect Vermont’s combined $2 billion aerospace and aviation industry with an $18 billion Québec aerospace cluster.

Vermont had the most significant state presence, with the largest delegation to date, featuring Governor Phil Scott and several Vermont businesses; BETA Technologies, Dynapower, G.S. Precision, Kaman Composites, Liquid Measurement Systems, North Country Engineering, Stephens Precision, Ten Fold Engineering.

Funding provided in part by the Vermont State Trade Expansion Program grant allowed these companies to participate in the conference and meet with large Canadian buyers, such as Bombardier, CAE, and Héroux-Devtek, as well as suppliers for new international business opportunities. This work is crucial to reconnect and rebuild supply chains following the pandemic.